ATO prioritising debt collection

As the economy emerges from COVID-19, the ATO is re-focusing on debt collection.

During the pandemic, the ATO deliberately shifted its focus away from firmer debt collection action to help and assist businesses and the community experiencing financial challenges because of the pandemic. It took a softly-softly approach, acknowledging the financial hardship that the virus wrought on business and individuals alike. However, with the economy now opening back up, business as usual on the ATO debt collection front, has now largely resumed.

That said, ATO Deputy Commissioner Vivek Chaudhary has confirmed that the ATO’s preferred approach is always to work with taxpayers to resolve their situation through engagement rather than enforcement.

“We have a range of support and assistance we can provide, and we can tailor a solution to a taxpayer’s unique circumstances. What is critical is that taxpayers or their representatives talk to us and respond to our calls.

We understand that a lot of people – especially small businesses – have done it tough through COVID and may now have a tax debt. Our message is – don’t stick your head in the sand – even if you can’t pay the full amount owed straight away, please contact us or your registered tax professional to discuss and we will work with you to set up an appropriate payment arrangement. We cannot help taxpayers who do not engage with us.”

Where taxpayers don’t engage, the ATO is taking firmer action. This includes garnishees, recovery of director penalties, disclosure of business tax debts, and legal actions including summons, creditors petition, wind-up and insolvency action.

The ATO has also recently written to businesses under two key awareness programs – disclosure of business tax debts and the use of Director Penalty Notices.

These programs focus on taxpayers who have not responded to calls and letters – and have significant tax obligations outstanding. The ATO to date has sent 29,552 awareness letters for disclosure of business tax debts and 52,319 awareness letters about the use of Director Penalty Notices (DPNs).

The disclosure of business tax debts measure allows the ATO to report significant tax debts (over $100,000) to Credit Reporting Bureaus (CRBs) under certain circumstances. The measure provides a new level of visibility of significant tax debts for the business community which will allow them to make more informed decisions. Debts subject to a formal dispute or an Inspector General of Taxation and Taxation Ombudsman investigation are not reported until the dispute or the complaint is resolved.

The DPN awareness program makes contact with directors whose company has not met their existing debts including PAYG(W), Superannuation Guarantee Charge and GST. Directors are notified of the ATO’s intent to issue a DPN which enables the ATO to commence recovery of the director penalty from each director of the company if the company does not actively manage their debt.

If you have an outstanding debt you should speak with us or call the ATO on 13 11 42 (8am to 6pm local time Monday to Friday).

Last minute trust distributions and record keeping

In late June, the ATO released their ‘100A guidelines’ provided in respect of the 2021/22 income year (‘Managing section 100A for the 2021–22 income year’).

In summary, the guidelines would appear to be a reiteration of previously published draft material (the 23 February Guidelines) with no or little direction with respect to the practical issues and determinations that taxpayers and their advisors will need to make with regards to the 2021/22 income year.

It is noted that the ATO is focused on practitioners implementing and maintaining substantive records to support the arrangements entered for 2021/22 or undertaken in respect of the matters in question. Keep good records that explain the transactions that have happened. Having a clear understanding as to why entitlements have been dealt with in the way they have will help support your position. It will also assist in timely resolution in the event that the ATO reviews your arrangement.

While each arrangement depends on its facts, the following will be important:

■ the trust deed (including amendments), trustee resolutions, and contact details of the trustee

■ for an inter-party loan, copies of the loan agreements and records of the purpose for making the loan

■ evidence to demonstrate that a beneficiary has received or enjoyed the benefit of their entitlement.

It is acknowledged that intra-family arrangements are typically conducted with a greater level of informality than commercial dealings that are conducted by unrelated parties. Nonetheless, to the extent possible, contemporaneous records should be maintained that demonstrate the objectives an arrangement was intended to achieve and how it helped to achieve them.

Going forward regarding future years, the ATO could not be clearer in its draft guidance about how it sees section 100A of the ITAA (1936) operating. Where a beneficiary receives and enjoys their present entitlement to trust income, section 100A will have no role to play.

However, where another person receives a payment or a benefit in relation to that present entitlement, and there was a purpose that someone pays less tax, there may be a reimbursement agreement and section 100A can apply. The beneficiary is then taken never to have been entitled to the distribution and the trustee is assessed under section 99A at the top marginal tax rate.

There is an exclusion for ‘ordinary family dealings’ which the ATO has sought to read down in its draft guidance.

The ATO’s interpretation is currently at odds with that of the Federal Court. The result of that ongoing litigation will be crucial.

Contact us if you have concerns or are in doubt with regards to the prospect of determining distributions to adult beneficiaries for the 2021-22 income year or the records that need to be maintained.

Super guarantee rises to 10.5%

The increase to the superannuation guarantee (SG) rate from 1 July 2022 will see more employees (and certain contractors) entitled to additional SG contributions on their pay. But what happens when income earned before 30 June is paid after 30 June 2022 – will employees be entitled to the higher SG rate of 10.5%?

SG based on when an employee is paid

On 1 July 2022, the SG rate increased from 10% to 10.5%. In some cases, an employee’s pay period will cross over between June and July when the rate changes.

However, the percentage employers are required to apply is determined based on when the employee is paid, not when the income is earned. The rate of 10.5% will need to be applied for all salary and wages that are paid on and after 1 July 2022, even if some or all of the pay period it relates to is before 1 July 2022.

This means if the pay period ends on or before 30 June, but the pay date falls on or after 1 July, the 10.5% SG rate applies on those salary and wages. The date of the salary and wage payment determines the rate of SG payable, regardless of when the work was performed.

EXAMPLE

Nicholas is an employee of ABC Pty Ltd.

If Nicholas performed work:

■ In June (or partly in June and partly in July) but he was paid in July, the SG rate is 10.5% on his entire payment and contributions totaling 10.5% of his ordinary time earnings for the September 2022 quarter must be made to his superannuation fund by 28 October.

■ In July but was paid in advance (before 1 July), the SG rate is 10% and contributions totaling 10% of his ordinary time earnings for the June 2022 quarter must be made to his superannuation fund by 28 July.

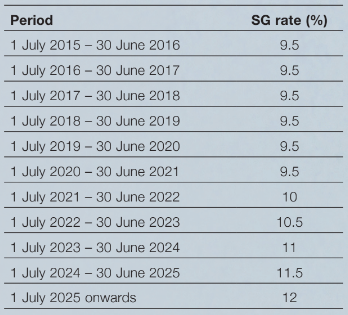

SG rate will continue to rise

With Labor elected, employers should prepare for ongoing, annual increases to the SG rate over the coming years. The following already-legislated increases to 12% by 2025 will proceed as follows:

Monthly $450 minimum threshold removed

A further change to the SG rules is that from 1 July 2022, the $450 per month minimum SG income threshold has been repealed. This means that employers will be required to make quarterly SG contributions on behalf of low-income employees earning less than $450 per month (unless another SG exemption applies).

Prior to 1 July 2022, an employer was not required to pay SG contributions for an employee who earned less than $450 per month.

This change is estimated to benefit approximately 300,000 people or 3% of employees1, who are mainly young and/or lower-income and part-time workers, where around 63% are female2. These changes will help these workers to start accumulating superannuation earlier as well as help address the gap in superannuation savings between women and men.

1: Estimates based on ATO Single Touch Payroll data for July 2019, provided to the Retirement Income Review, published in the Retirement Income Review – Final Report. Canberra: Commonwealth of Australia, 2020, pp 298, 301

2: Ibid, pp 45, 300-301

ATO tax time focus for small business

The ATO has released a tax time tool kit to assist businesses and us as your tax advisor to nail your 2021/22 business tax return.

The ATO has also flagged what it will be focusing on for small business tax returns for 2021–22:

■ deductions that are private in nature and not related to business income, as well as overclaiming of business expenses (especially for taxpayers running a home-based business)

■ omission of business income, for example income from the sharing economy or new business ventures

■ record keeping – including insufficient or non-existent records that are needed to substantiate claims.

ATO Assistant Commissioner Andrew Watson said:

We know it’s been a tough couple of years for many small business owners, and we understand your tax obligations may not be at the top of your list. So, if you need a hand, I encourage you to contact your registered tax professional.

No matter what your situation is, it’s never too late to ask for help. Tax time is also a great time to discuss ATO debts with your registered tax professional and set up a payment plan if you need one.

Income

Mr. Watson reminded small businesses to include all income, including earnings from ‘side hustles’.

Small businesses should include all income in their income tax return, including cash, coupons, EFTPOS, online, credit or debit card transactions, and income from platforms such as PayPal, WeChat or Alipay.

The ATO has also reminded businesses that most government payments or financial support received as a result of COVID-19 needs to be included as taxable income, whereas some others are exempt and should not be included. The ATO has detailed information listing how all support payments should be treated on its website. Speak to us for further guidance.

Deductions

Mr. Watson reminded businesses to only claim what they are entitled to, and that their business structure affects their entitlements and obligations. The way that sole traders, partnerships, trusts, and companies claim deductions is often different.

There are three golden rules for what the ATO accepts as a valid business deduction:

■ the expense must have been for your business, not for private use

■ if the expense is for a mix of business and private use, you can only claim the portion that is used for your business

■ you must have records to prove it.

Lodgment deadlines

Although tax returns are generally due by 31 October, because you are lodging with us (a registered agent), you will have more time to prepare and lodge. This will generally be in the first half of 2023.

Scam myths

In the past 12 months, the ATO has identified and taken action against 595 websites impersonating its online services. These fake sites are designed to steal passwords, personal information and identity documents, such as passports and driver licences.

Currently, the ATO is seeing many SMS and email scams leading to fake myGov sign-in pages –more than 360 of these scams have reported to the ATO since April 2022. However, there many different types of tax and super scams happening year-round, not just in the lead up to Tax Time.

Scammers are always looking for new ways to convince unsuspecting taxpayers into divulging personal information, such as bank details, usernames and passwords.

This year, the ATO has taken out the guesswork and busted some scam myths to help people stay protected:

Myth 1 – Only older people fall for scams

In the past three years, younger Australians have fallen victim to the most tax scams. In 2021, people aged 25 to 34 reported the most amount of money lost to tax scams, closely followed by those aged 18 to 24. In contrast, those aged 55 and above were among those who reported the least financial losses to the ATO. The ATO’s Assistant Commissioner Tim Loh says:

We want Gen Z and Millennials to know they need to watch out too, as they are just as susceptible to falling for scams, especially those that involve fake tax debts or threats about alleged fraud

If you get a phone call saying it’s from the ATO and it doesn’t sound right, hang up. Check in with someone you trust, like your registered tax agent.

Even better go to the ATO’s website where we have a listing of all the current ATO scams or call us on our dedicated scam hotline 1800 008 540.

Myth 2 – Scams are easy to spot, you’d be a fool to fall for one!

“Email and SMS scams are not always full of typos, bad grammar, and promises of riches from foreign royalty. We are seeing many more sophisticated scam messages using official language and fraudulent websites that mimic online services” Mr Loh said.

“We’ve seen some very convincing email and SMS scams that would trick even the most cautious people.”

The ATO does send emails and SMS to taxpayers to share general information or reminders, or to ask people to check their myGov inbox or get in touch with them.

However, here are some tell-tale signs to look out for if an email or SMS says it’s from the ATO. The ATO will never:

■ send an unsolicited message requesting personal information via a return email or SMS,

■ send an email or SMS with a link to log in to their online services,

■ ask you to pay a fee in order to receive a refund.

Myth 3 – Scams only happen during tax time

While you may only focus on your tax when it’s time to lodge, scammers are constantly looking for ways to steal your personal details and financial information.

The ATO sees different types of tax and super scams happening year-round.

It’s important to always stay vigilant to potential scams, and to keep your personal and financial details safe.

Some common year-round scams involve scammers:

■ phoning people about a fake tax debt, and threatening that they’ll be arrested if they don’t pay it straight away

■ sending texts to people saying that they’re suspected of being involved in cryptocurrency tax evasion. If you receive this text, don’t click on the link.

■ sending emails impersonating the ATO and asking for people to update their financial information so their tax refund can be processed.

Contact us if you are unsure about the legitimacy of tax or super communications with another party.

STP year-end finalisations … due soon!

Employers need to make STP finalisation declarations by 14 July each year. As your registered agent, we can assist you in this important, upcoming process.

If you have 20 or more employees, you should be reporting closely-held (related) payees each pay day along with arms-length employees. The finalisation due date for closely-held payees is 30 September each year.

A ”closely-held (related) payee” is an individual directly related to the entity from which they receive payments (for example, family members of a business, directors or shareholders of a company, or beneficiaries of a trust).

For small employers (19 or fewer employees) who only have closely-held payees, the due date for end-of-year STP finalisation will be the payee’s income tax return due date.

For an employer with a mixture of both closely-held payees and arms-length employees, the due date for end-of-year STP finalisation for closely-held payees is 30 September each year. All other employees are due 14 July each year.

Before making your finalisation declaration, make sure your STP information is correct. If you can’t make a finalisation declaration by the due date, you will need to apply for a deferral. We can take this up for you.

You can finalise your data earlier if it’s ready. The sooner you finalise your employees’ information, the sooner they will be able to lodge their tax returns for 2021/22.

This finalisation process is explained in detail in the STP employer reporting guidelines, including amendments for current and previous financial years. As noted, we can assist you in this process.

When you have reported and finalised your employees’ information through STP, you are exempt from:

■ providing payment summaries to your employees

■ lodging a payment summary annual report.

For payments to your employees that were not reported through STP, you still need to:

■ give a payment summary to your employees

■ provide the ATO with a payment summary annual report for these payment summaries.

If you identify that you need to make an amendment after you have submitted a finalisation declaration, you’ll need to submit these as soon as possible. You can make the amendments to finalised STP data in your STP solution.

The ATO recommend you tell your employees when you make an adjustment that will be reflected in their income statement. If they have already lodged their tax return they may need to lodge an amendment.

You will need to tell your employees:

■ you are no longer required to provide them with a payment summary for the information you’ve reported and finalised through STP

■ they can access their year-to-date and end-of-year income statement online through myGov or talk to their registered tax agent

■ ‘income statement’ is the new term for their payment summary (if they don’t already know this from last year)

■ to wait until their income statement is ‘Tax ready’ before lodging their tax return

■ to check their personal details and if necessary, update with both you and the ATO (incorrect personal details may prevent them from seeing their STP information).

If an employee does not have a myGov account, they can easily create one online. They can also talk to their tax agent who will have access to their income statement information.

Accessing your super early

The key purpose of superannuation is to provide individuals with benefits for their retirement, which is when most people will access their superannuation savings. But, in some cases, individuals may be able to access some of their superannuation early upon meeting certain eligibility rules.

Common conditions of release

A condition of release must be met before you can access your superannuation benefits. The most common conditions of release for paying benefits are when you:

■ Have reached your preservation age and retire (see below for preservation age)

■ Have reached your preservation age and begin a transition-to-retirement income stream

■ Cease an employment arrangement on or after the age of 60

■ Turn 65 years of age (even if you haven’t retired)

■ Pass away.

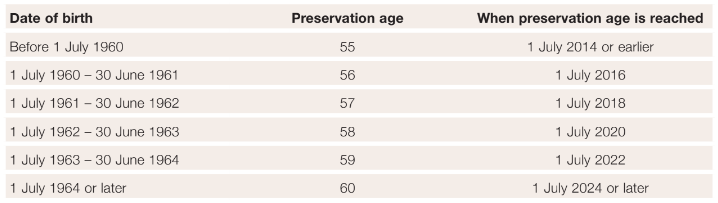

Preservation age

Access to superannuation benefits is generally restricted to individuals who have reached their preservation age. This is because the preservation rules aim to prevent early access to benefits.

The table below summarises when you may reach your preservation age and therefore potentially access your superannuation benefits:

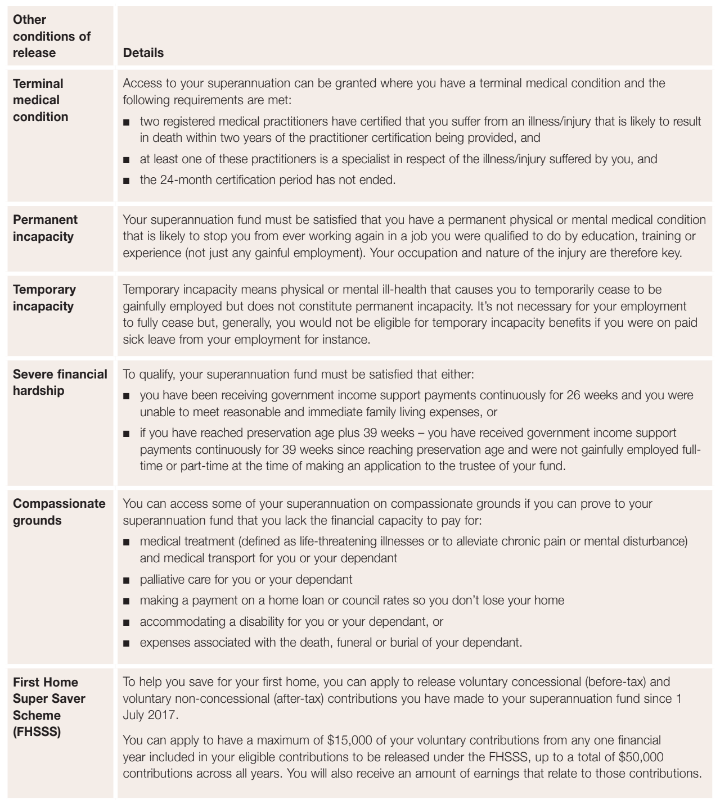

Other conditions of release

Besides the common condition of release events that apply to most cases, there are other special circumstances where at least part of your superannuation benefits can be released before you have reached preservation age.

Need more information?

There are many factors to consider before accessing your superannuation, including how it will impact your retirement, taxation and what effect it will have on any other benefits you’re receiving.

Please contact us if you would like more information on any of these conditions of release and would like to discuss your options. We will explain the conditions and requirements that need to be met to demonstrate your eligibility which may help you access your superannuation benefits.